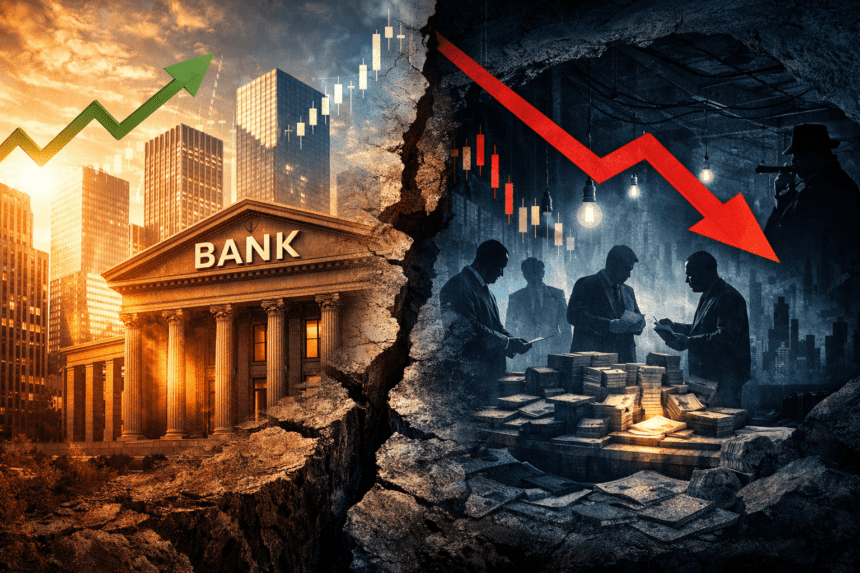

Wall Street did not kill credit risk after 2008. It may have just pushed it into a darker corner of the market.

The post-2008 banking story was supposed to be about safety. Banks were meant to deleverage, clean up balance sheets, and reduce the kind of risks that nearly detonated the financial system in the Global Financial Crisis. But the latest warning is more unsettling: a large share of that risk may not have disappeared at all. It may have simply migrated into the shadow-lending world of private credit, nonbank finance, and opaque funding chains.

That is the core argument behind the latest market anxiety. Banks have moved the equivalent of roughly 18 million BTC into shadow lenders, pointing to around $1.3 trillion in bank lending tied to nondepository financial institutions. Federal Reserve data show loans to nondepository financial institutions have indeed climbed to around $1.9 trillion in early 2026, while Fed research published in 2025 also highlighted how commitments to other nonbank financial institutions had surged to about $2.2 trillion after years of rapid growth.

That does not automatically mean another 2008-style collapse is imminent. But it does suggest the fault line may have moved. Instead of risk sitting squarely on bank balance sheets, more of it now runs through private credit funds, securitization vehicles, and other nonbanks that are typically less transparent and less tightly regulated than traditional lenders. The IMF and other stability watchers have repeatedly warned that the rapid growth of nonbank finance is creating new vulnerabilities for the global financial system.

The timing matters. Private credit has grown into a roughly $2 trillion market, and concerns around that sector have become harder to ignore in recent weeks. Reuters reported that investors have questioned valuations in Blue Owl’s private credit portfolio, while fund withdrawal limits and markdowns elsewhere have added to the feeling that the sector has not yet been tested by a full credit cycle. MarketWatch also reported that major banks now carry sizable private-credit exposure, and UBS has warned that the space still has not faced a true stress event.

This is why the “shadow lender” issue matters beyond finance insiders. When lending migrates from regulated banks to less visible credit channels, the system can look safer on the surface while becoming harder to map underneath. The New York Fed has argued that banks and nonbanks are not clean substitutes but deeply interconnected, with nonbanks often relying heavily on bank funding, credit lines, and back-end support. That means stress in private credit may not stay neatly contained inside private credit.

Regulators are clearly paying attention. The Bank of England this week proposed tougher liquidity readiness reforms, shaped in part by lessons from Silicon Valley Bank and Credit Suisse, while Australia’s Reserve Bank said nonbank lenders and private credit firms have increased credit availability but could also contribute to higher loan losses ahead, even if their current systemic footprint remains smaller than the banks’.

The real warning here is not that history will repeat in the exact same way. It is that finance has a habit of shifting risk to wherever oversight is lighter, liquidity looks plentiful, and investors are willing to believe the plumbing is stronger than it really is. In 2008, that illusion shattered in housing linked credit. In 2026, the market is increasingly wondering whether the next crack could begin in private credit and the wider nonbank lending web surrounding it. That is not the same crisis. But it rhymes.

For Bitcoin and crypto watchers, the deeper angle is simple. If shadow-credit stress triggers a broader liquidity event, risk assets will not get a free pass just because they sit outside the banking system. In a genuine funding squeeze, correlation rises, leverage unwinds, and investors sell what they can. The banking system may look better capitalised than it was in 2008, but the question now is whether the next scare has already been outsourced.